ESMO Breast Cancer 2024 – Olema digs deep to declare victory

Plenty of questions remain about the latest palazestrant data drop as investors hope for a Novartis buyout.

Plenty of questions remain about the latest palazestrant data drop as investors hope for a Novartis buyout.

At the tail end of last year Olema Oncology came off worse in a battle of the SERDs, but the company is fighting back. Updated results from a phase 1/2 study of its contender palazestrant plus Novartis’s CDK4/6 inhibitor Kisqali in breast cancer, released today, initially sent the group’s stock up 7% this morning.

However, there are several reasons to be cautious, which could explain why these gains were wiped out a few hours later. Firstly, while Olema noted that 50 patients had been treated, more than half of these were missing from efficacy analyses. Furthermore, most patients so far have been second or third line, but Olema is planning to test this combo in phase 3 in first-line disease.

The company didn’t give too many details of that upcoming pivotal trial, but did concede that it will need more funds to start it. The latest data in ER-positive, HER2-negative disease, which are set to appear in a poster tomorrow at the ESMO Breast Cancer meeting, will only fuel speculation that Olema could be acquired by Novartis.

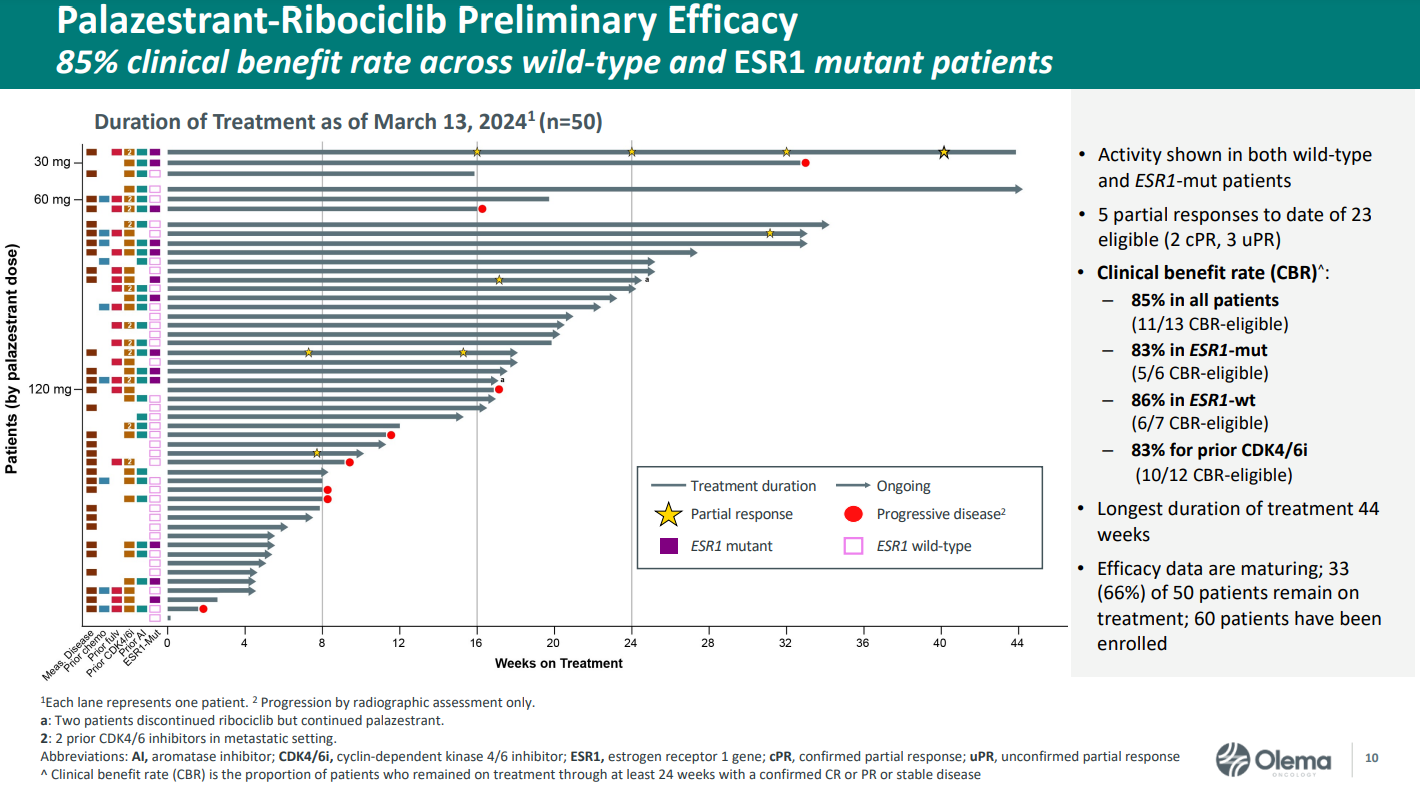

ORR 22% or 10%?

According to Olema, there were five partial responses among 23 evaluable patients, giving an overall response rate of 22%. On the face of it, this looks better than the single partial response seen among 19 patients last year.

However, the company did not specify on what basis the other 27 patients were excluded from the latest analysis, and had not responded to a request for clarification from ApexOnco at the time of publication. If a denominator of 50 is used, this gives a much less impressive ORR of 10%. In addition, three of these five responses were unconfirmed at the data cutoff of 13 March.

Olema also highlighted a clinical benefit rate of 85%, representing the proportion of patients with stable disease or better for at least 24 weeks. Similarly, though, this analysis only included 13 patients – those who enrolled 24 weeks or more before data cutoff, and received at least one cycle of palazestrant.

Although the company compared the data with other SERD studies, which cast palazestrant in a favourable light, it’s difficult to glean much from these results, given the small number of patients involved.

Olema said it hoped to provide more data from the trial later this year or in early 2025. The next update could include the full 60 patients enrolled – 10 were excluded from today’s tolerability analysis because they’d been on treatment for less than four weeks.

First line

Some of these new patients received palazestrant plus Kisqali first line, Olema’s chief executive, Sean Bohen, noted during a conference call today. Investors and potential suitors alike will no doubt be keen to see how these fare – in the latest data drop 74% of patients had received prior therapy.

Another thing to keep an eye on will be how the combo fares in ESR1 mutants versus wild-types – so far, it has shown activity in both. Efficacy with other SERDs has largely been limited to ESR1m patients, and Olema puts palazestrant’s broad efficacy here down to it being a complete oestrogen receptor antagonist (Ceran), not just a degrader.

Olema is also evaluating palazestrant monotherapy in second/third-line disease, in the phase 3 Opera-01 trial, results from which are due in 2026.

Bohen today played down the possibility of also testing the Kisqali combo in later-line settings, noting that most patients would now be receiving the Novartis drug first line at it becomes the CDK4/6 inhibitor of choice.

As such, Olema looks canny for plumping for this combination in contrast, for example, to Arvinas, which has tied up with Pfizer and its waning CDK4/6 inhibitor Ibrance. Although Olema previously tested palazestrant alongside Ibrance this is no longer a priority, Bohen noted.

With the company now betting squarely on a Kisqali combo, Olema will have to hope that it can do enough to convince Novartis to pull the trigger on a deal.

1652